September non-agency CMBS surges post Labour Day.

Steve Baumgartner, Oct 2025 - 4 min read

Steve Baumgartner, Oct 2025 - 4 min read

Image source: Unsplash

Non-Agency CMBS market overview

As anticipated, the non-Agency Commercial Mortgage-Backed Security (CMBS) market came roaring back after Labor Day. Specifically, this CMBS market analysis reveals $13.6 billion in September issuance, marking the second-highest month for the year. Deal flow rebounded sharply as refreshed market participants executed on the pipelines they’d been building through August’s quiet period.

Notably, the market’s momentum accelerated as the month progressed. The final two weeks saw 12 deals for $9.1 billion in non-Agency come to market. Additionally, two Commercial Real Estate (CRE) Collateralised Loan Obligations (CLOs) totalled $1.5 billion. This surge in supply was met with continued spread tightening. Therefore, this underscores the depth of investor demand and the market’s ability to absorb significant volume without indigestion.

Total non-Agency CMBS issuance through September reached $92.3 billion. This continues to significantly outpace last year, which was $76.1 billion through the same period. Consequently, this represents a robust 21% increase, underscoring the market’s sustained strength.

Source: Commercial Mortgage Alert, Morningstar Credit

Stepping back, trailing twelve-month non-agency CMBS issuance now totals $127.0 billion. This maintains a $10.6 billion monthly pace. Moreover, the market has clearly found its post-April rhythm. The last five months delivered consistently strong volumes. Thus, this demonstrates the resilience and stability that issuers and investors have been seeking.

Source: Commercial Mortgage Alert, Morningstar Credit

Deal composition analysis

Single asset single borrower (SASB)

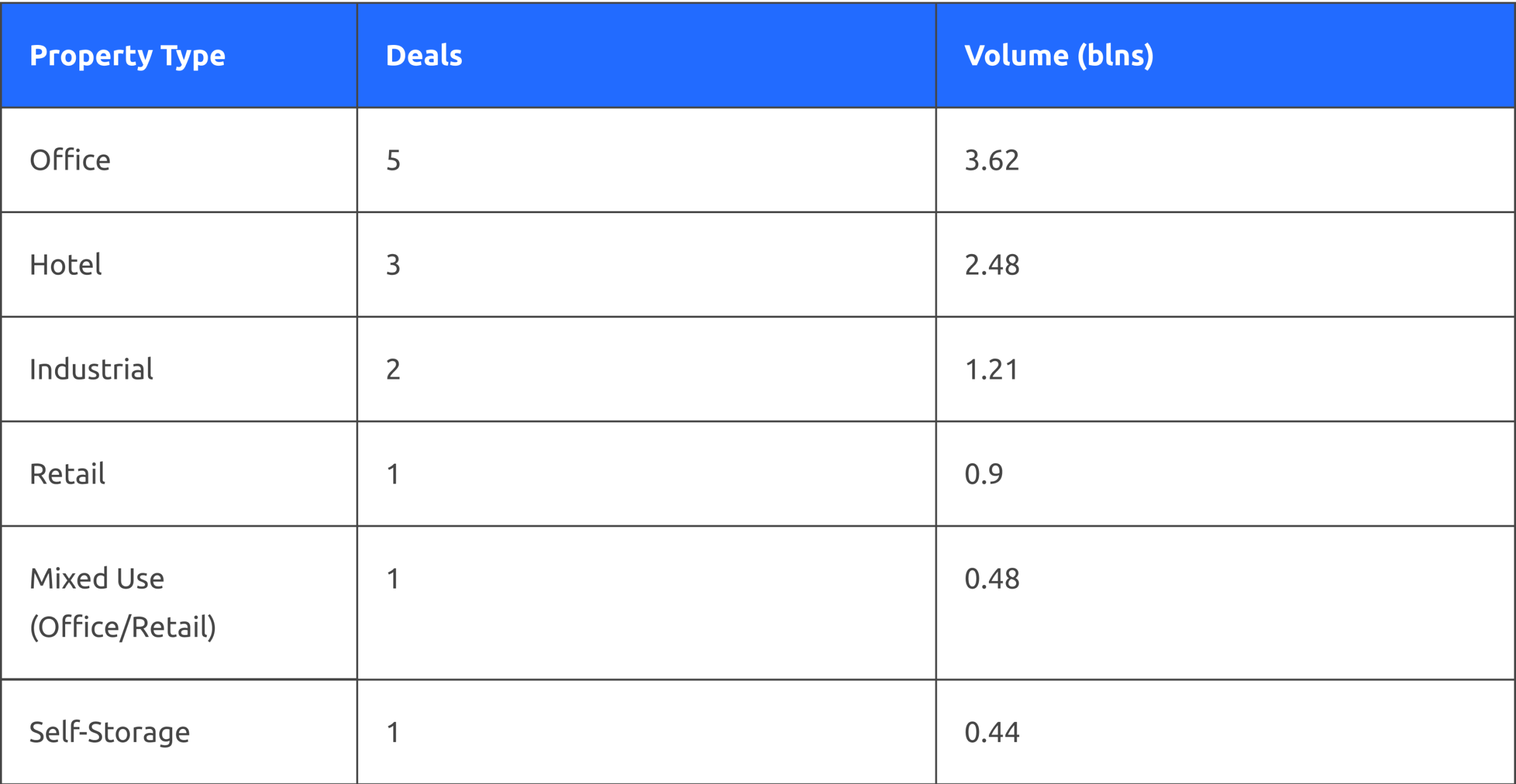

SASB deals continued their dominance in September with 13 transactions totalling $9.1 billion. This represents roughly two-thirds of the month’s issuance. Furthermore, the month showcased the breadth of investor appetite across property types. These ranged from trophy office towers to extended-stay hotel portfolios.

The September SASB property mix was:

Office properties dominated both deal count and volume. Specifically, five transactions totalled $3.6 billion. These were headlined by two Manhattan trophy towers: the $1.4 billion refinancing of 11 Madison Avenue and the $1.25 billion financing of Five Manhattan West. Moreover, these marquee assets, along with Boston’s Hub on Causeway mixed-use development, demonstrate institutional-grade office properties in gateway markets continue to command significant investor appetite.

Hotels showed impressive strength with three deals totalling $2.5 billion. The massive $1.9 billion Blackstone/Starwood Extended Stay America portfolio refinancing led this segment. Notably, this covered 220 properties across 33 states, representing the largest single deal of the month.

.

Conduit deals

The conduit market delivered its best performance in over a year. Specifically, six September deals totalled $4.5 billion. For the first time in 2025, a conduit deal surpassed $1 billion. Additionally, deal sizes averaged a healthy $746 million across the month.

Yet September’s strength underscores rather than solves the conduit market’s fundamental challenge. With monthly volumes ranging from $1.4 billion to $4.5 billion over the past year, the market remains trapped in a feast-or-famine pattern. Therefore, this reflects the difficulty of aggregating loans for conduit execution in today’s environment.

Source: Commercial Mortgage Alert, Morningstar Credit

CRE CLO market

The CRE CLO market’s remarkable year continued. Year-to-date issuance reached $23.1 billion through September. Consequently, this further solidifies the asset class’s recovery. This year’s volume has already surpassed the combined total for the previous two years, which was $15.4 billion.

September saw two deals totalling $1.5 billion late price in the month. This keeps pace with the market’s steady momentum. Furthermore, the transactions featured healthcare-backed collateral and a diversified pool. This adds to the variety of property types accessing the CRE CLO market this year. Both transactions were priced in the final weeks. This is consistent with the seasonal pattern of back-loaded activity as market participants returned from summer breaks.

Source: Commercial Mortgage Alert, Morningstar Credit

Market analysis and outlook

Credit and spread environment

New issue CMBS spreads continued their tightening trend in September, even as the market absorbed significant supply during the month’s final two weeks. With 14 deals totalling over $10.6 billion in non-Agency and CRE CLOs pricing in just the last two weeks of September, the market demonstrated remarkable depth and investor appetite. Deals across all product types saw strong execution with reports indicating strong demand across the board. This robust demand, despite heavy supply, underscores both the quality of collateral coming to market and investors’ confidence in the broader credit environment.

September surge sets the stage for Q4

September’s $13.6 billion performance validated the optimism expressed in August about post-Labor Day pipelines. The market returned from the summer break refreshed and ready to execute, delivering the second-highest monthly total of 2025. The backloaded nature of activity was striking, with nearly 80% of the month’s volume pricing in the final two weeks as deals came together in rapid succession. Investors demonstrated their capacity to absorb this concentrated wave of supply without disruption.

The conduit market’s resurgence deserves particular attention. After months of inconsistent execution, September’s six deals totalling $4.5 billion, including the first billion-dollar conduit transaction of 2025, raises the question of whether this represents a turning point or simply another data point in the ongoing volatility. Time will tell, but the improved execution suggests lenders are making progress in the challenging work of aggregating loans for conduit structures.

Fed policy as a catalyst

As expected, the Federal Reserve delivered its first rate cut in nine months in September, reducing the federal funds rate by 25 basis points and signalling additional cuts ahead. This shift in monetary policy provided a boost to market sentiment, with the CMBS market responding positively to the improving rate outlook. Lower rates ease refinancing pressures for borrowers facing maturity walls and improve deal economics for new issuance, creating a more favourable environment for both sponsors and investors.

The path forward appears increasingly accommodative, with market participants anticipating further rate reductions through year-end and into 2026. This evolving rate environment should provide continued tailwinds for CMBS issuance, potentially driving even stronger volumes in the fourth quarter as borrowers look to lock in financing ahead of further market shifts.

Forward-looking considerations

With robust pipelines heading into the fourth quarter and trailing twelve-month issuance at $127.0 billion, the fundamentals point toward a strong finish for 2025. Year-over-year growth of 21% through September positions the market for what could be its best annual performance since the pre-GFC era.

Positive drivers:

- Fed rate cuts creating more favourable refinancing environment and improved deal economics

- Continued spread tightening demonstrating robust investor demand despite heavy supply

- Conduit market showing signs of improved execution and larger deal sizes

- CRE CLO market momentum continuing with over $23 billion issued this year

- Trophy office properties proving that quality real estate and strong sponsorship trump negative sector sentiment

Risk factors:

- Headline and policy risk from D.C. creating uncertainty around trade and regulatory guidelines

- Ongoing geopolitical uncertainties that could impact credit markets

- Persistent office-sector-specific challenges despite strong execution for premium properties

- Potential market volatility if economic data disappoints or Fed policy shifts unexpectedly

Conclusion

September’s strong performance reflects a CMBS market operating at full strength. With $92.3 billion year-to-date, 21% year-over-year growth, and the added catalyst of Fed rate cuts, the market appears positioned to deliver its best annual performance since the pre-GFC era. The ability to absorb over $10 billion in the final two weeks of September while maintaining tight spreads and strong execution demonstrates remarkable market depth and investor confidence.

With three months remaining and strong forward pipelines, 2025 is tracking toward the CMBS market’s best performance in over a decade. The momentum is real, the fundamentals are sound, and the stage is set for a strong finish to 2025.