2026 Launches with $15.7 billion in non-agency CRE securitisation.

Steve Baumgartner, Feb 2026 - 5 min read

Steve Baumgartner, Feb 2026 - 5 min read

Market overview

The non-agency commercial real estate securitisation market delivered a robust start to 2026 with $15.7 billion in combined issuance, led by an exceptional CRE CLO performance. Non-Agency CMBS contributed $8.2 billion across 13 deals while CRE CLOs added $7.5 billion across 7 transactions, nearly one-quarter of 2025’s entire CLO volume issued in a single month.

Non-agency CMBS market overview

January’s $8.2 billion in non-Agency CMBS issuance represents a 4.5% increase over January 2025’s $7.9 billion, maintaining the momentum established in 2025 and validating the optimistic 2026 projections. Deal flow was steady throughout the month with strong forward-looking pipelines, suggesting the market’s $170-185 billion combined target remains well within reach.

Source: Commercial Mortgage Alert, Morningstar Credit

Deal composition analysis

Single Asset Single Borrower (SASB)

January’s 10 SASB deals totalling $5.6 billion demonstrated continued investor appetite across diverse property types, with hospitality and office properties leading monthly activity. The headline transaction was Blackstone and Starwood Capital’s $1.87 billion Extended Stay America portfolio refinancing covering 196 hotels across 29 states, marking the third refinancing from their 2021 acquisition and the largest SASB deal of the month.

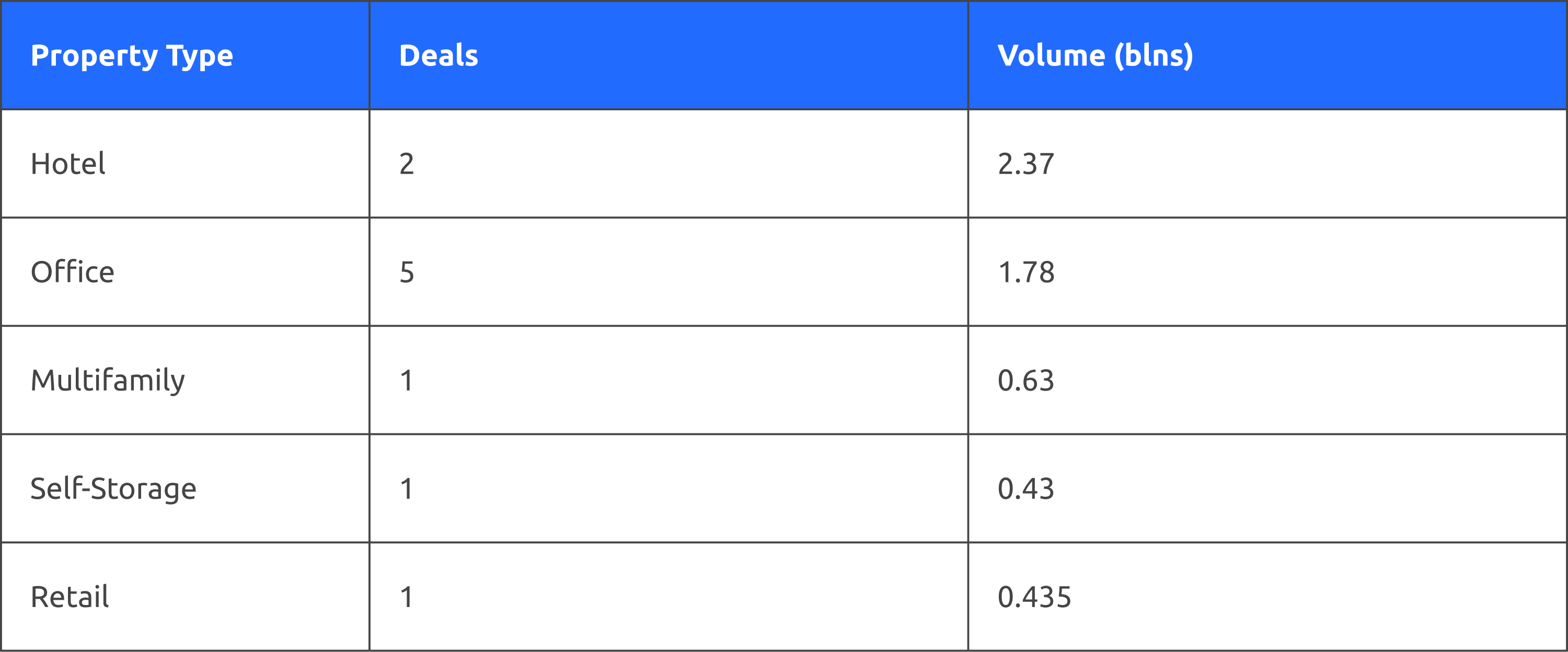

The January SASB property mix was:

Office properties accounted for five transactions totalling $1.8 billion, with notable activity in Manhattan including Vornado’s refinancings of One Park Avenue ($525 million) and 7 West 34th Street ($250 million), alongside SL Green’s acquisition financing of Park Avenue Tower ($480 million). The continued execution of quality office assets in gateway markets reinforces the bifurcation theme established in 2025 whereby institutional-grade properties with strong tenant rosters continue to find ready capital.

Hotels, while represented by only two deals, dominated volume at $2.4 billion, driven by the massive Extended Stay America transaction alongside Lone Star’s $500 million refinancing of six full-service hotels across four states.

Source: Commercial Mortgage Alert, Morningstar Credit

Conduit deals

January’s conduit market delivered three deals totalling $2.4 billion, providing a measured start to 2026. While representing fewer transactions than in recent months, the average deal size of $784 million demonstrates continued ability to aggregate loans on a meaningful scale when market conditions align.

The conduit performance reflects the ongoing reality of this market segment. Execution quality remains solid when deals come to market, but monthly volumes continue to vary based on loan aggregation dynamics rather than investor demand. The steady pipeline visibility into February suggests lenders remain committed to bringing collateral pools to market throughout the first quarter.

CRE CLO market

January’s CRE CLO performance was nothing short of exceptional, with seven deals totalling $7.5 billion, which was nearly one-quarter of 2025’s entire annual volume. This remarkable start underscores the asset class’s momentum coming out of 2025’s strong $30.5 billion year.

The strong execution across all seven transactions demonstrates robust investor appetite for floating-rate CRE exposure, with managers bringing diverse collateral pools to market and achieving favourable pricing. This early momentum, combined with the pipeline visibility discussed at CREFC, suggests the CRE CLO market has firmly established itself as a vital financing channel for transitional commercial real estate.

Source: Commercial Mortgage Alert, Morningstar Credit

Market analysis and outlook

Credit and spread environment

The non-agency CRE securitisation market entered 2026 with exceptional momentum. Aggressive investor demand drove spreads tighter across all product types, with deals heavily oversubscribed throughout January.

Execution was consistently strong, with spreads tightening from initial guidance and many tranches achieving significant oversubscription. The strength was evident in both new issue execution and secondary market pricing, with the favourable conditions that characterised late 2025 appearing to have accelerated into the new year.

Post-CREFC momentum

January’s performance validates the optimism expressed at CREFC in early January. The record attendance and positive sentiment observed at the conference translated directly into market activity, with strong pipeline visibility extending into February and beyond. The combination of available capital, improving rate expectations, and operational confidence has created conditions conducive to sustained issuance throughout the first quarter.

Forward-looking considerations

With $15.7 billion achieved in January and strong pipeline visibility into February, the market is tracking well ahead of the pace needed to reach the $170-185 billion combined target for 2026. While January benefited from deals that had been in process during the December holiday period, the sustained momentum and favourable execution conditions suggest the market has genuine strength rather than just pent-up activity.

The key factors supporting continued strength include stable-to-improving rate expectations, robust investor demand demonstrated by spread tightening and oversubscription, and diverse deal flow across SASB, conduit, and CRE CLO channels providing multiple paths to market for issuers.

Conclusion

January’s $15.7 billion performance demonstrates that 2025’s momentum has carried into the new year with strength. Consistent investor demand, tightening spreads, and diverse deal flow across all product types validate the optimistic CREFC projections and position the market firmly on track toward the $170-185 billion target.

The CRE CLO market’s exceptional start, delivering nearly one-quarter of 2025’s annual volume in a single month, signals potential for significant growth beyond last year’s strong totals. CMBS execution remains strong across both SASB and conduit channels, with February pipelines indicating sustained activity ahead.

The question entering 2026 was whether the market could build on its recovery. January’s performance provides a clear answer: the fundamentals, capital, and execution are aligned for meaningful expansion.