July Non-Agency CMBS Issuance Beats the Heat

Steve Baumgartner, Aug 2025 - 4 min read

Steve Baumgartner, Aug 2025 - 4 min read

Non-Agency CMBS Market Overview

July 2025 Commercial Mortgage-Backed Security (CMBS) issuance defied typical summer seasonality, posting the second-highest monthly total of the year. Despite the calendar turning to traditional summer holidays and festivities, the U.S. non-agency CMBS market kept rolling along. Specifically, the market saw $12.4 billion in new paper come to market. This spread across an impressive roster of 20 deals. Consequently, this kept market professionals busier than ever during what is typically a quiet period.

Source: Commercial Mortgage Alert, Morningstar Credit

Digging in a bit deeper, data from Morningstar Credit shows the total trailing twelve-month non-agency CMBS issuance was just under $125 billion. This yields an impressive $10.4 billion average monthly. This is even more remarkable when you consider that these figures include April’s paltry $3.3 billion figure. At that time, the market digested the impacts of “Liberation Day” tariffs and the potential of a global trade war.

Moreover, the ability to quickly digest and respond to such events further demonstrates the resilience of the primary markets.

Source: Commercial Mortgage Alert, Morningstar Credit

Deal Composition Analysis

Single Asset Single Borrower (SASB)

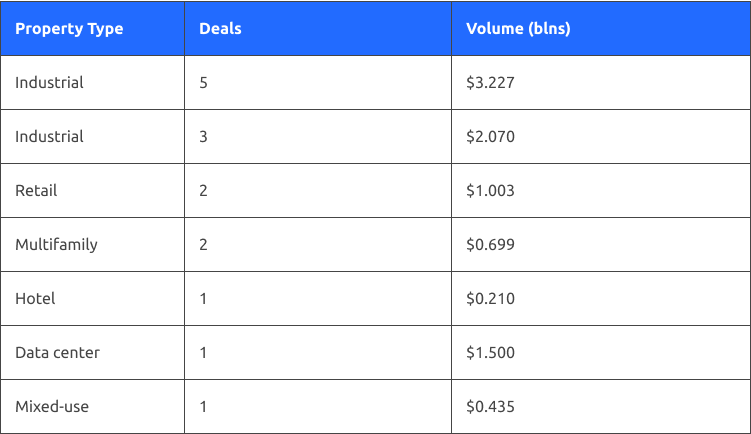

Unsurprisingly, SASB issuance continued its dominance in July 2025 CMBS issuance. Specifically, industry analysis from Trepp indicates they represented 75% of the deals by count and 74% by volume. Consequently, investors continue to snap up SASB paper.

Interestingly, July’s SASB issuance essentially represented all the major property types:

The diversity across property types showcases investors’ appetite for high-quality CRE assets regardless of sector. Furthermore, even well-positioned office properties with high-quality sponsors can achieve competitive financing by tapping the CMBS markets.

Conduit Deals

Not to be left behind, July saw five conduit deals priced for over $3.2 billion in new paper. This was the first time five conduits were priced in a month since March of this year. However, the average deal size in July was only $645 million. In contrast, in March it was $873 million. This illustrates how difficult it can be for lenders to aggregate and issue conduit paper at scale.

Nevertheless, all reports say that the conduits were well subscribed, and pricing was strong. Therefore, perhaps that will lead to increased deal sizes in the future.

Source: Commercial Mortgage Alert, Morningstar Credit

CRE CLO Market

In a repeat of June, just a single CRE CLO came to market in July for $960 million. While the monthly volume seems modest, aggregate issuance for 2025 now stands at $18.2 billion. Specifically, this is 2.1 times the total in 2024. Consequently, this highlights this product’s place as an alternative financing source for transitional assets.

Source: Commercial Mortgage Alert, Morningstar Credit

Market Analysis and Outlook

Credit and Spread Environment

The CMBS markets continue to demonstrate their strength and resilience. This persists despite ongoing noise from D.C. and macro pressures alongside sector-specific issues as commercial real estate continues to rapidly evolve.

Moreover, CMBS spreads have continued to tighten alongside strong deal execution. This showcases demand for high-quality paper with compelling relative value to corporate credit.

Summer Strength Defies Seasonality

July 2025 CMBS issuance surprisingly strong performance, achieving the second-highest monthly total for the year, challenging traditional issuance patterns. Specifically, the ability to continue strong issuance in the middle of summer demonstrates the strength of the market.

Furthermore, the pipelines indicate this pattern is set to continue in August, historically the quietest month of the year. Therefore, this sets the stage for an exciting end to the year.

Forward-Looking Considerations

With year-over-year growth exceeding 29% and trailing twelve-month issuance almost surpassing $125 billion, the market is well positioned for its best performance since pre-GFC.

Positive Drivers:

- Strong forward-looking pipelines with no signs of a slowdown ahead

- Tight execution patterns illustrated by strong pricing and oversubscription rates

- Conservative underwriting and high-quality assets lead to robust demand

Risk Factors:

- Potential August disruption due to investor pull-back and seasonal patterns

- Continued refinancing pressures due to a mismatch between current rates versus existing coupons, leading to more maturity defaults

- Sector-specific pressures, like office headwinds, as utilization continues to evolve

Conclusion

July 2025 CMBS issuance represents a watershed moment. Specifically, it positions the non-agency CMBS markets for their strongest year since the GFC while maintaining superior underwriting standards.

If the market can continue to capitalize on its momentum, the question will shift from whether the new normal can be maintained to how high the ceiling might be.