Non-Agency CMBS Maintains Strong Momentum in October

Steve Baumgartner, Nov 2025 - 4 min read

Steve Baumgartner, Nov 2025 - 4 min read

Image source: Unsplash

Non-Agency CMBS Market Overview

The non-Agency CMBS market maintained its strong momentum in October with $11.5 billion in issuance across 15 deals, demonstrating consistent execution as the fourth quarter progressed. Unlike September’s back-loaded surge, October’s activity was spread more evenly throughout the month, reflecting a market operating at a steady, sustainable pace.

Total non-Agency CMBS issuance through October reached $103.8 billion, positioning the market to surpass 2024’s full-year total of $106 billion within weeks. The year-over-year comparison through October remains impressive, with 2025 running 16% ahead of last year’s $89.6 billion pace through the same period.

Source: Commercial Mortgage Alert, Morningstar Credit

Looking at the trailing twelve months, non-agency CMBS issuance reached $122.3 billion, keeping a $10.2 billion monthly run rate. October’s performance continues the pattern of reliable execution that has defined the second half of 2025, showcasing a market that has found its sustainable stride.

Source: Commercial Mortgage Alert, Morningstar Credit

Deal Composition Analysis

Single Asset Single Borrower (SASB)

Twelve SASB deals totaling $8.8 billion drove the majority of October’s non-Agency CMBS issuance, capturing over 75% of monthly volume. The array of property types accessing the market reflected the enduring principle that quality assets with institutional backing find receptive capital markets.

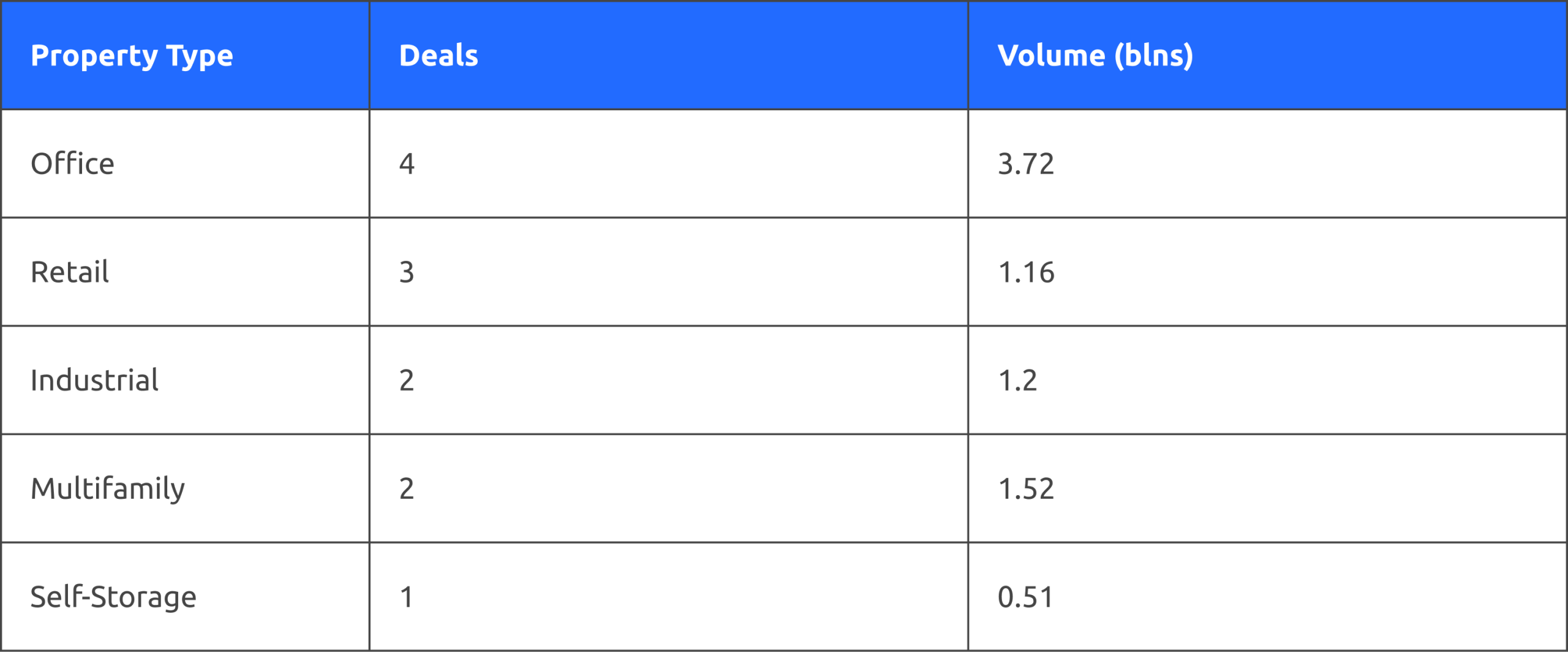

The October SASB property mix was:

Office properties once again led both deal count and volume with four transactions totaling $3.7 billion, continuing the trend of strong execution for quality assets with institutional sponsorship. The absence of hotel deals this month marks a notable shift from recent months where hospitality properties featured prominently, while multifamily and retail showed increased activity with $1.5 billion and $1.2 billion respectively.

Conduit Deals

The conduit market’s improved momentum continued in October with three deals totaling $2.7 billion, including a $1.3 billion transaction from the BMARK shelf, the largest conduit deal of 2025. The remaining deals, sized at $714 million and $689 million, saw strong execution with solid investor interest.

October’s solid execution continues to demonstrate that when lenders can successfully aggregate loans, there’s robust investor demand for conduit paper. While month-to-month volumes remain variable, the quality of execution and pricing encourages the remainder of 2025.

Source: Commercial Mortgage Alert, Morningstar Credit

CRE CLO Market

The CRE CLO market delivered two deals totaling $2.2 billion in October, each sized at $1.1 billion. Year-to-date issuance now stands at $25.3 billion, further cementing this year’s status as a full recovery year for the asset class.

October’s consistent deal sizing reflects a maturing market with established investor demand. The CRE CLO market continues to demonstrate its evolution into a reliable financing channel for commercial real estate, with strong execution carrying through the fourth quarter.

Source: Commercial Mortgage Alert, Morningstar Credit

Market Analysis and Outlook

Credit and Spread Environment

New issue CMBS spreads remained range-bound in October, trading stable to slightly wider across the stack as investors digested mixed signals from the Federal Reserve. Despite the modest spread widening, deal execution remained solid with consistent investor demand, though perhaps with slightly more caution than the aggressive appetite seen in prior months. The market’s ability to absorb $11.5 billion while maintaining orderly pricing demonstrates the underlying strength of investor conviction in quality collateral.

Fed Policy Creates some Near-Term Uncertainty

The Federal Reserve delivered its expected 25 basis point rate cut in October, but Fed Chair Jerome Powell’s subsequent comments tempered market enthusiasm. Powell’s indication that a December rate cut was “far from certain” introduced a note of caution into the rate outlook, contributing to the modest spread widening observed during the month. This shift from the September narrative of multiple cuts ahead creates some near-term uncertainty, though the broader accommodative trend remains intact.

Approaching a Milestone

With $103.8 billion year-to-date through October, the non-Agency CMBS market stands poised to surpass 2024’s full-year total of $106 billion in early November. This milestone will underscore 2025’s status as a true recovery year and positions the market for one of its strongest annual performances since the pre-GFC era.

Forward-Looking Considerations

Despite the compressed timeframe heading into year-end with the holiday season approaching, market sentiment remains constructive. Strong forward pipelines and sustained momentum suggest the market can deliver a solid finish to 2025, even as participants navigate Fed policy uncertainty and typical year-end dynamics.

Positive Drivers:

- Year-to-date volume at $103.8 billion positioning market to exceed 2024’s full-year total

- Consistent execution across all product types demonstrating market depth

- Conduit market showing improved execution quality and investor reception

- CRE CLO market continuing strong performance with over $25 billion issued this year

- Quality real estate with institutional sponsors maintaining strong investor appeal

Risk Factors:

- Fed policy uncertainty following Powell’s comments dampening expectations for December rate cut

- Compressed year-end timeline with holiday season approaching

- Spreads widening modestly as investors reassess rate outlook

- Ongoing geopolitical uncertainties that could impact credit markets

- Persistent office-sector-specific challenges despite strong execution for premium properties

Conclusion

October’s consistent performance reflects a CMBS market that has found its rhythm. With $103.8 billion year-to-date and momentum carrying into the final stretch, 2025 is on track to surpass last year’s total within weeks and deliver the market’s strongest annual performance in over a decade.

While Fed Chair Powell’s cautious stance on additional rate cuts introduces some near-term uncertainty, the fundamentals remain sound. Strong pipelines, solid execution across all product types, and sustained investor demand position the market well for the final two months of 2025. The year that began with questions about sustainability is now poised to deliver definitive answers.