Non-Agency CMBS Market Exceeds 2024 Volume with Month to Spare

Steve Baumgartner, Sep 2025 - 10 min read

Steve Baumgartner, Sep 2025 - 10 min read

Image source: Pexels

Non-Agency CMBS Market Overview

The non-Agency CMBS market reached a significant milestone in November, surpassing 2024’s full-year total of $106 billion in the first week of the month. November’s $12.4 billion in issuance brought year-to-date volume to $116.2 billion, positioning 2025 to deliver the strongest annual performance since 2007 with one month remaining.

Activity remained robust through most of November, with issuance spread evenly until the Thanksgiving holiday effectively closed the market for the final two working days of the month. The month’s volume of $12.4 billion represents a 33% increase over November 2024’s $9.4 billion, marking the fourth-highest monthly total for 2025.

Source: Commercial Mortgage Alert, Morningstar Credit

The year-over-year comparison is impressive, with 2025 running 20% ahead of last year’s $97 billion pace through November. The acceleration has been particularly pronounced in the second half of the year, with the market demonstrating exceptional strength following April’s trade policy-driven pause. From May through November, the market has delivered consistently strong volumes, more than making up for the spring disruption.

Over the trailing twelve months, non-agency CMBS issuance now stands at $125.3 billion, maintaining a healthy $10.4 billion monthly average. The market has demonstrated remarkable consistency throughout 2025, with the milestone achievement in early November underscoring the sustained execution that has characterized this recovery year.

Source: Commercial Mortgage Alert, Morningstar Credit

Deal Composition Analysis

Single Asset Single Borrower (SASB)

Nine SASB deals totaling $9.6 billion represented the core of November’s non-Agency CMBS issuance, accounting for over three-quarters of monthly volume. The month was notable for the outsized $3.5 billion Blackstone data center financing, the largest single SASB transaction of 2025.

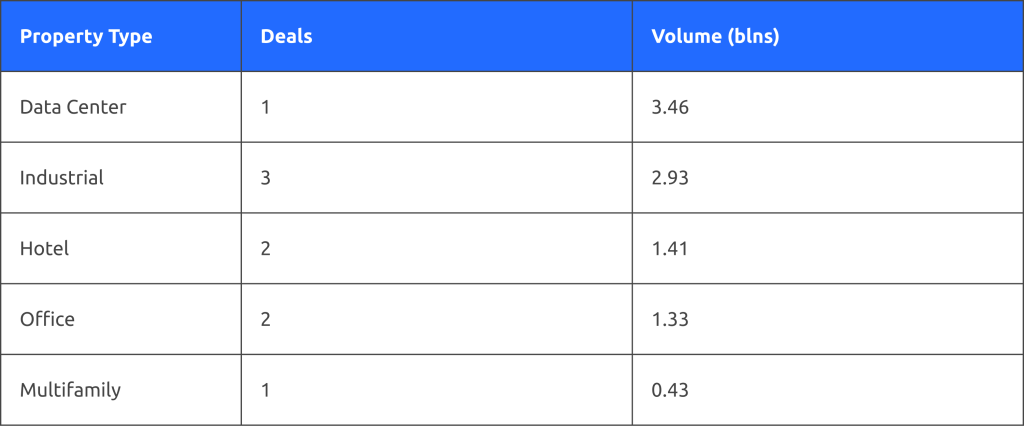

The November SASB property mix was:

Industrial properties showed particularly strong activity with three deals totaling $2.9 billion, while the single data center transaction dominated monthly volume. Office and hotel properties each contributed two deals, demonstrating continued investor willingness to back quality assets across property sectors. The absence of retail from November’s mix marks a shift from recent months, though the overall diversity underscores the market’s broad-based strength.

Conduit Deals

November’s conduit activity pulled back to two deals totaling $1.5 billion after October’s stronger showing. While the reduced volume reinforces the ongoing challenges in consistent loan aggregation for conduit execution, deal flow remained orderly with solid investor reception.

Specialty Deals

Of particular note was the emergence of specialty product types that have been largely absent from 2025’s issuance. November marked the first appearance of seasoned collateral deals this year, with two transactions totaling $790 million. Both deals, the first from Santander ($502 million) and second from Cross River Bank ($288 million), securitized multifamily and mixed-use loans originally intended to be held on balance sheet but later brought to market.

Additionally, November featured one lease-backed deal for $493 million, the third such transaction this year following October’s two deals totaling $659 million. The appearance of these specialty products, particularly the balance sheet loan securitizations, signals banks’ willingness to tap the CMBS markets for liquidity and capital management, adding another dimension to 2025’s diverse issuance landscape.

Source: Commercial Mortgage Alert, Morningstar Credit

CRE CLO Market

The CRE CLO market delivered a strong November with five deals totaling $4.3 billion, the second-strongest monthly performance of the year for the asset class. Year-to-date issuance now stands at $29.6 billion, firmly establishing 2025 as a watershed year for CRE CLO recovery.

November’s deals came from a diverse group of sponsors, including Starwood Property Trust ($1.1 billion), Bridge Investment Group ($1.2 billion), LaSalle Investment Management ($1.0 billion), Lument ($664 million), and A10 Capital ($350 million). The collateral remained heavily weighted toward multifamily properties, with bridge loans and transitional financing continuing to dominate the underlying portfolios. The strong execution across all five transactions underscores the sustained investor appetite for floating-rate CRE exposure and the CRE CLO market’s maturation into a reliable financing channel.

With $29.6 billion year-to-date, 2025 has already approached 2022’s full-year volume of $30 billion. While still well below the 2021 peak of $45 billion, this year’s performance represents a remarkable recovery from the lean years of 2023-2024, when combined annual issuance totaled just $15.4 billion.

Source: Commercial Mortgage Alert, Morningstar Credit

Market Analysis and Outlook

Credit and Spread Environment

New issue CMBS spreads remained largely stable in November, with pricing holding steady across most product types, though there was some marginal widening in conduit deals. Strong investor demand and solid execution characterized the month, with the market demonstrating its ability to absorb significant volume, including the $3.5 billion Blackstone data center financing without disruption. The stable pricing environment underscores the depth of capital available for quality commercial real estate transactions.

Fed Policy Creates some Near-Term Uncertainty

The Federal Reserve faces its final meeting of 2025 this month amid unusual uncertainty. While markets widely expect a third quarter-point rate cut, the six-week government shutdown left Fed officials without critical October economic data, forcing them to make policy decisions with an incomplete picture. Chair Powell’s October warning about “driving in the fog” has proven prescient.

Internal divisions have emerged within the committee as both inflation and unemployment have risen simultaneously, creating conflicting pressures on the Fed’s dual mandate. For CMBS markets, the prospect of continued easing provides support heading into December, though the lack of policy clarity creates some near-term uncertainty.

December Outlook: A Strong Finish

The final month of 2025 is shaping up to deliver an impressive conclusion to an exceptional year. The first week of December alone saw approximately $8.3 billion in deals either announced or priced, with market participants anticipating one of the strongest December performances on record during the first two to three weeks before the holiday slowdown. Strong pipelines and sustained investor appetite position the market to add meaningful volume to an already historic year.

Forward-Looking Considerations

With $116.2 billion issued through November and robust December activity underway, 2025 is poised to deliver the non-Agency CMBS market’s strongest annual performance since 2007. The year’s achievement, surpassing 2024’s full-year total with well more than a month to spare after recovering from April’s trade policy disruption, represents a definitive statement about the market’s resilience and continued relevance as a financing channel for institutional commercial real estate.

Positive Drivers:

- December pipeline set to deliver one of the strongest end-of-year finishes on record

- Year-to-date volume at $116.2 billion, exceeding 2024 already

- CRE CLO market approaching $30 billion, closing in on 2022 levels

- Consistent execution across all product types, demonstrating market depth

- Quality assets with institutional sponsors, maintaining strong investor demand

Risk Factors:

- Fed policy uncertainty with internal divisions and incomplete economic data

- Compressed holiday timeline limiting execution window in late December

- Political pressure on Fed chair, potentially creating policy volatility in 2026

- Rising inflation and unemployment creating conflicting economic signals

- Persistent sector-specific challenges despite strong execution for premium properties

Conclusion

November’s achievement of surpassing 2024’s full-year total represents more than just a numerical milestone, it reinforces the CMBS market’s return to prominence as a vital financing channel for commercial real estate. With $116.2 billion year-to-date and December poised to add significant volume, 2025 is delivering the market’s strongest performance since 2007.

The year’s narrative arc, from April’s trade policy disruption through the sustained strength of the second half, demonstrates the market’s resilience and maturity. Strong execution across SASB, conduit, and CRE CLO products, combined with the emergence of specialty transactions like seasoned collateral deals, underscores the breadth and depth of today’s CMBS market.

As December unfolds with what appears to be record pre-holiday activity, 2025’s success story continues to be written. The fundamentals remain sound, pipelines are strong, and the market has definitively answered any lingering questions about its sustainability and relevance.